Amazon delivered a strong Q1 2026 earnings report, and the cleanest way to read it is this: the operating business beat expectations in exactly the places investors care most about right now.

Revenue came in above expectations. AWS re-accelerated meaningfully. Advertising kept growing like a second high-margin engine. Retail profitability also improved. The one major caveat is that the headline EPS beat looked better than the underlying operating story because net income was boosted by a large Anthropic-related non-operating gain.

The Short Version

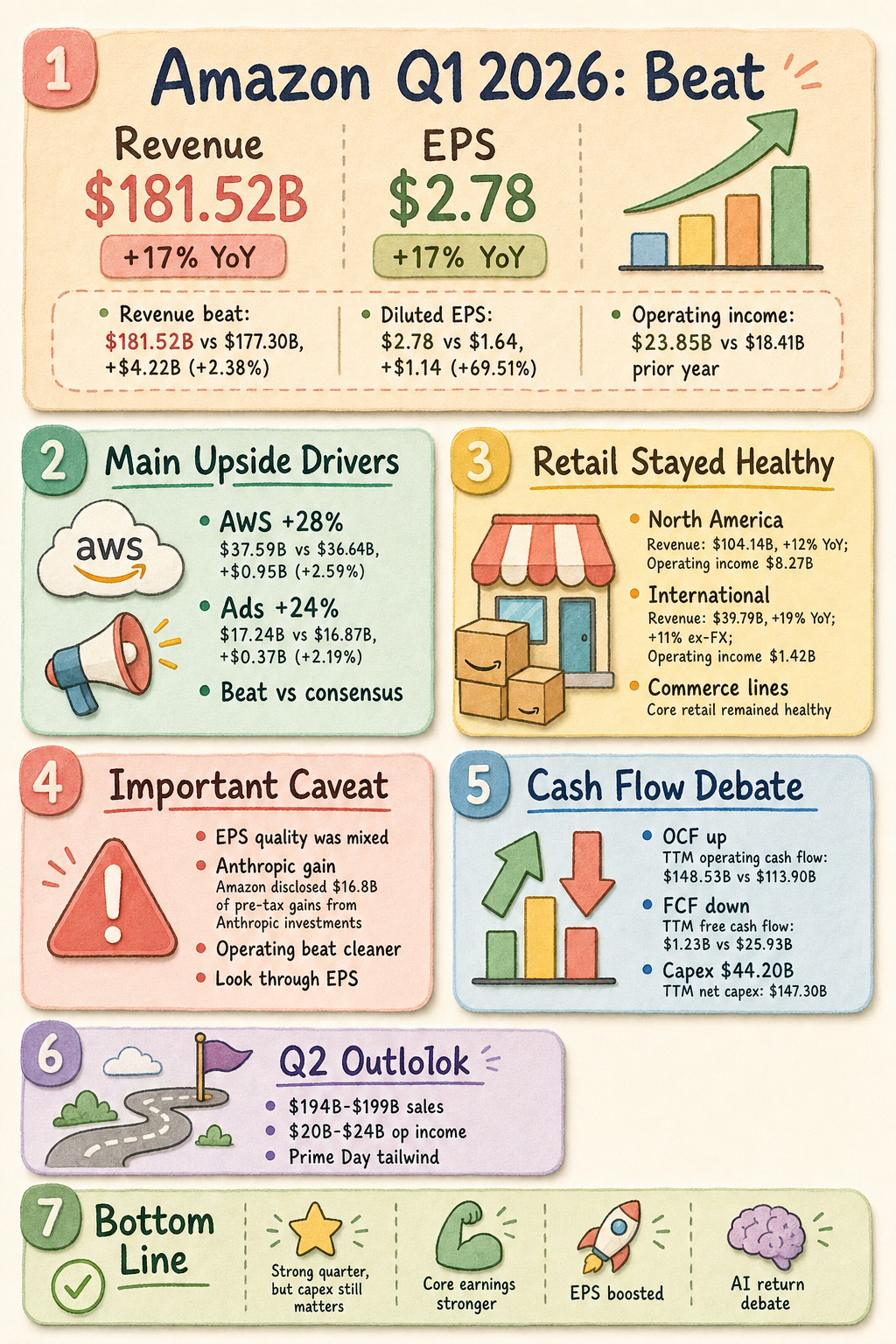

- Revenue beat: Amazon reported $181.52 billion in Q1 revenue, ahead of the roughly $177.30 billion expectation cited in market coverage.

- AWS was the main upside driver: AWS revenue reached $37.59 billion, up 28% year over year, and marked its fastest growth in 15 quarters.

- Advertising stayed strong: Advertising revenue hit $17.24 billion, up 24% year over year, reinforcing Amazon’s shift toward faster-growing and higher-margin businesses.

- Operating performance was high quality: Operating income reached $23.85 billion, above both expectations and the high end of company guidance.

- EPS quality was mixed: Diluted EPS of $2.78 was helped by $16.8 billion of pre-tax non-operating gains tied to Amazon’s Anthropic investment.

- Capex is still the central debate: operating cash flow is surging, but free cash flow remains compressed because Amazon is spending aggressively on AI and data center capacity.

What Amazon Actually Reported

The headline consolidated results were strong across the board:

- Revenue: $181.52 billion, up 17% year over year

- Operating income: $23.85 billion, up from $18.41 billion

- Operating margin: 13.1%, up from 11.8%

- Net income: $30.26 billion, up from $17.13 billion

- Diluted EPS: $2.78, up from $1.59

Segment performance showed why the market responded well:

- North America revenue: $104.14 billion, up 12%

- International revenue: $39.79 billion, up 19%

- AWS revenue: $37.59 billion, up 28%

- AWS operating income: $14.16 billion

- AWS operating margin: 37.7%

That AWS number matters most. At Amazon’s scale, a 28% growth rate sends a much stronger signal than a generic “cloud was solid” narrative. It suggests enterprise AI demand is large enough to move the needle materially, and that Amazon is participating meaningfully rather than just defending share.

Why AWS Matters So Much Here

For Amazon, AWS is still the strategic center of the investment case.

The market can tolerate huge infrastructure budgets if it believes those dollars are being converted into durable revenue, operating profit, and customer commitment. Q1 moved that argument in Amazon’s favor.

A few things stand out:

- Growth re-accelerated visibly. AWS at 28% year over year was the fastest growth pace in 15 quarters.

- Profitability remained excellent. A 37.7% AWS operating margin gives Amazon room to keep investing while still producing substantial earnings power.

- AI demand is no longer theoretical. Strong AWS results fit the broader 2026 market pattern: investors are rewarding hyperscalers that can show AI demand is already showing up in real cloud revenue.

This is why the AWS beat matters more than the headline EPS beat.

Advertising Keeps Getting More Important

Advertising may be the most underappreciated part of the quarter.

Amazon’s advertising services revenue reached $17.24 billion, up 24% year over year, and also beat expectations. That matters because ads are not just a growth story. They are a mix-shift story.

As advertising becomes a larger part of Amazon’s revenue base, it strengthens the company’s margin profile and makes the overall business more resilient. The combination of AWS plus advertising gives Amazon two powerful profit engines beyond the core retail narrative.

The EPS Beat Needs a Footnote

This was a strong quarter, but it is important not to overread the bottom line.

Amazon disclosed $16.8 billion of pre-tax gains in non-operating income tied to its Anthropic investment. That means the EPS beat should not be interpreted as fully operating in nature.

The cleaner hierarchy is:

- Revenue beat: high quality

- AWS beat: high quality

- Operating income beat: high quality

- EPS beat: real, but materially boosted by investment-related gains

That distinction matters because future quarters may not get the same help from mark-to-market or observable price adjustments tied to strategic investments.

The Other Big Debate: Capex vs Free Cash Flow

The bullish and cautious interpretations of Amazon both show up clearly in the cash flow statement.

On the positive side:

- Q1 operating cash flow: $26.03 billion

- TTM operating cash flow: $148.53 billion, up from $113.90 billion

On the more cautious side:

- TTM free cash flow: $1.23 billion, down from $25.93 billion

- Q1 property and equipment purchases: $44.20 billion

- TTM property and equipment purchases: $151.00 billion

In plain English, Amazon is generating a lot more cash from operations, but it is also spending at an extraordinary rate to build AI and data center capacity.

That keeps the core investor question alive: how quickly will this capex convert into durable free-cash-flow growth?

The quarter did not resolve that debate, but it did make the pro-investment case easier to defend because AWS performance suggests the demand side is real.

Guidance Looked Constructive Too

Amazon guided for Q2 2026:

- Net sales: $194 billion to $199 billion

- Operating income: $20 billion to $24 billion

That outlook suggests the company still sees healthy demand and continued profitability even while investment intensity remains elevated. It also leaves room for calendar support from Prime Day timing.

My Read

This looked like a high-quality operating beat with a lower-quality EPS headline.

That is still a good quarter.

If you strip away the accounting noise from the Anthropic-related gain, the real message is that Amazon’s core thesis improved:

- AWS is re-accelerating

- advertising is compounding

- retail profitability is holding up better than many expected

- management is spending heavily because it sees a large AI opportunity

The remaining question is not whether Amazon had a good quarter. It did.

The real question is whether today’s extreme capex intensity will translate into tomorrow’s durable free-cash-flow expansion. That is the key issue investors will keep testing over the next several quarters.

Bottom Line

Amazon’s Q1 2026 report strengthened the bull case on core operations. Revenue, AWS, advertising, and operating income all came in better than expected, which is exactly what investors wanted to see from a company spending aggressively into the AI infrastructure cycle.

The caveat is that EPS was materially helped by Anthropic-related non-operating gains, so the bottom-line beat was not as clean as the operating beat.

Overall, though, this was a constructive quarter. Amazon showed that its AI and cloud investment story is tied to real demand today, not just a promise about tomorrow.

Sources

- Amazon IR quarterly results page: https://ir.aboutamazon.com/quarterly-results/default.aspx

- Amazon Q1 2026 earnings release: https://s2.q4cdn.com/299287126/files/doc_earnings/2026/q1/earnings-result/AMZN-Q1-2026-Earnings-Release.pdf

- Amazon Q1 2026 10-Q: https://d18rn0p25nwr6d.cloudfront.net/CIK-0001018724/e5b7de6a-55b0-4300-b981-4e5a8857972d.pdf

- SEC filing HTML: https://www.sec.gov/Archives/edgar/data/1018724/000101872426000014/amzn-20260331.htm

- Amazon earnings coverage page: https://www.aboutamazon.com/news/company-news/amazon-earnings-q1-2026-report

- CNBC earnings coverage: https://www.cnbc.com/2026/04/29/amazon-amzn-q1-earnings-report-2026.html

- CNBC AWS coverage: https://www.cnbc.com/2026/04/29/aws-earnings-q1-2026.html